If you are thinking about buying your first home in Orange County and your family is telling you to wait because of the war with Iran, that concern is understandable. Global conflict can affect oil prices, inflation expectations, financial markets, and mortgage rates. Those are not abstract issues. They can change affordability fast.

But that still does not mean this is automatically a bad time to buy a home in Orange County.

The better question is not whether the headlines are unsettling. The better question is whether waiting is likely to improve your outcome. For many first-time buyers looking in places like Irvine or Tustin, while also comparing more affordable options farther north, that is the question that matters most.

Right now, the Orange County housing market looks more pressured than broken. Rates have moved higher from recent lows, which hurts payment. At the same time, inventory has improved, buyers have more choices than they had during the frenzy years, and the local market is still functioning. That means the decision to buy now or wait should be based less on fear and more on your budget, time horizon, and how this specific market is behaving.

Why This Question Is Coming Up Right Now

When people hear about conflict involving Iran, the housing concern usually starts with energy. Iran matters to global oil markets, and when there is fear of supply disruption, oil prices can move higher. Higher energy prices can feed inflation worries. Inflation worries can push bond yields up. Mortgage rates often follow.

That chain reaction is why the Iran conflict has become part of real estate conversations, even here in Orange County.

This does not automatically turn into a housing crash. It does mean volatility matters. A first-time buyer who was comfortable with one payment at one rate may suddenly be looking at a noticeably different monthly cost a week or two later. That is real. But it is different from saying the market has stopped working or that buyers should all move to the sidelines.

How the Iran Conflict Can Affect Housing Without Crashing the Market

The most realistic way to explain this is simple: the conflict matters because it can put upward pressure on rates and uncertainty on decision-making.

That matters in three ways.

First, higher rates reduce affordability. A buyer who qualifies comfortably one month may feel squeezed the next.

Second, uncertainty can make some buyers pause. When consumers feel nervous about the economy, they often delay major decisions, especially a first home purchase.

Third, it can keep the Federal Reserve cautious if inflation remains sticky. The Fed does not set mortgage rates directly, but inflation expectations and bond markets have a major influence on them.

So yes, the conflict matters. But a geopolitical shock affecting housing through rates is not the same thing as a wave of distressed inventory, forced selling, or collapsing local demand. Those are very different conditions, and Orange County is not currently showing signs of that kind of breakdown.

What Mortgage Rates Are Doing, and Why Buyers Feel It Immediately

One reason this topic feels so personal is that rate changes hit buyers faster than almost anything else. Even a modest move upward can increase a monthly payment enough to change what feels comfortable.

That is why waiting for a better rate sounds appealing. But rate timing is not easy. Buyers often assume the Federal Reserve will cut, mortgage rates will fall, and affordability will improve in a straight line. Housing rarely works that cleanly.

Mortgage rates are influenced by inflation, bond yields, labor market data, and investor sentiment. So even if the Fed eases later, rates can still remain volatile. And if rates do move lower in a meaningful way, that can bring more buyers back into the market, which may increase competition.

For buyers in Orange County, the practical takeaway is this: a future lower rate is possible, but it is not guaranteed, and it may not arrive in a way that makes buying easier overall.

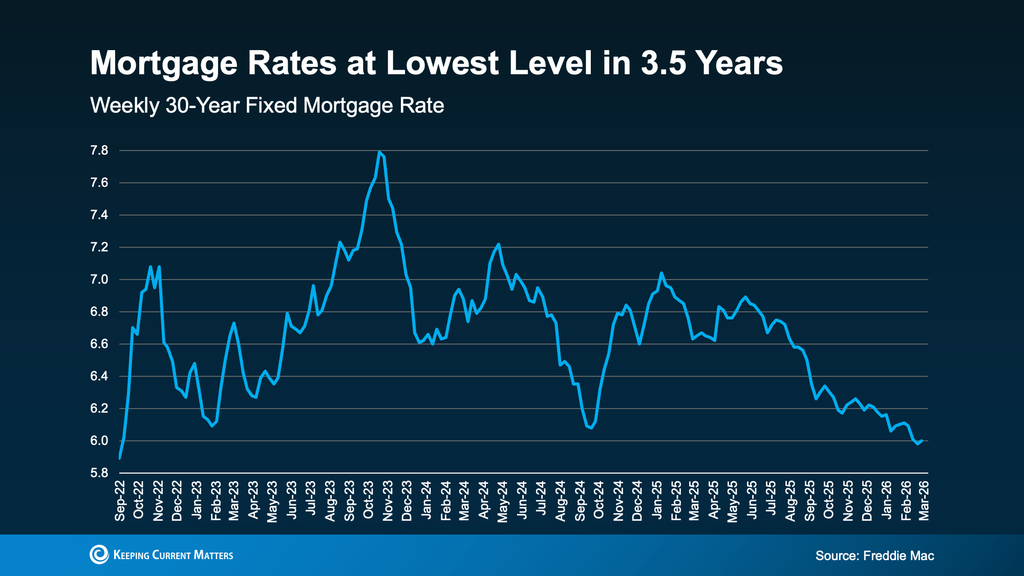

Mortgage rates recently reached their lowest point in 3.5 years before rising again after the Iran conflict. Even with that increase, rates remain below year-ago levels.

The Orange County Market Is Slowing From Frenzy, Not Falling Apart

This is where local data becomes more useful than national fear.

Orange County active inventory rose from 3,687 in mid-March to 3,866 by the end of March. Demand also rose, from 1,639 pending sales to 1,654, but inventory grew faster than demand. As a result, expected market time moved from 67 days to 70 days.

That is not what a collapsing market looks like.

It looks more like a market that is becoming more balanced. Buyers have more choices. Sellers have more competition. The pressure is still there, but the conditions are less frantic than the ultra-competitive years when low rates and low supply created constant urgency.

For first-time buyers, that change matters. A more balanced market can create room to compare homes more carefully, negotiate more often, and avoid chasing every listing with the same level of desperation buyers felt during the hottest pandemic years.

There is also an important product-type difference. Attached homes such as condos and townhomes have been moving slower than detached homes in Orange County, giving many first-time buyers a little more room to evaluate options. In the late-March local data, expected market time for attached homes was 77 days versus 67 days for detached homes. For many first-time buyers, that can create a better opening because entry-level attached homes may offer a little more breathing room than the detached market.

Why This Market May Be Better for Patient First-Time Buyers Than the Headlines Suggest

The local sold data paints a more nuanced picture than the headlines do.

In Orange County’s February 2026 sold data, 57% of homes closed below original list price, 14% closed at original list price, and 29% closed above original list price. That tells us two important things at the same time.

First, well-positioned homes can still attract aggressive offers.

Second, this is not a market where everything automatically sells over asking.

That is actually encouraging for thoughtful buyers. It means pricing still matters. Timing still matters. Negotiation still matters. A first-time buyer who is pre-approved, realistic about payment, and selective about value may have a better shot today than in a market where every decent listing is swarmed instantly.

That does not make the market easy. It makes it more rational.

What Waiting Could Look Like for a Buyer

This is the part most buyers really want answered.

Waiting can help in some situations. If you are still building savings, improving credit, paying down debt, or trying to create a more comfortable monthly budget, waiting can be smart. Buying before you are ready just because you are tired of renting is not a great strategy.

But waiting is not automatically protective.

If mortgage rates fall, more buyers may jump back in, which can make the market more competitive. If prices continue to appreciate, even modestly, a lower future rate may be offset by a higher purchase price. If rates stay elevated longer than expected, then the hoped-for improvement may not arrive on your timeline.

That is why the real risk of waiting is not just “maybe prices go down.” The real risk is that you spend six to twelve months hoping for a cleaner setup and end up facing the same or higher home prices, only with more buyer competition if rates improve.

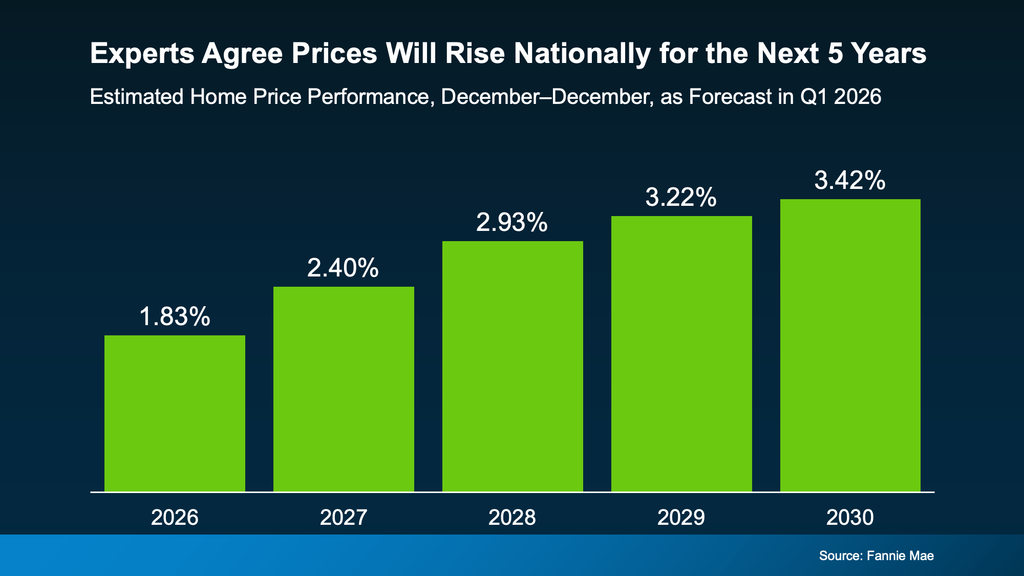

That matters because national price forecasts still do not look anything like a crash scenario. Fannie Mae’s Q1 2026 expert survey projected home prices to rise each year through 2030, with moderate annual gains rather than a steep reset. That does not guarantee every Orange County neighborhood moves the same way, but it reinforces the broader point: waiting only pays off if your personal finances improve or the monthly payment gets meaningfully better, not just because you expect a national price drop.

For many first-time buyers in Orange County, the best comparison is not buying now versus some imaginary perfect market. It is buying now versus what the next six to twelve months might realistically look like.

Why This Is Different From COVID and Other Headline-Driven Housing Moments

A lot of housing expectations were distorted by COVID.

During that period, rates collapsed, demand surged, preferences changed quickly, and the market became unusually aggressive. Many people still compare today’s housing conditions to that environment, but it was not normal.

Today’s market is different. Borrowing costs are higher than they were during the COVID years, but rates were still below last year’s level before rising again as the Iran conflict added pressure. Sellers still have an advantage in many neighborhoods, but not in the same way. Buyers are more payment-sensitive. Inventory is improving, but not flooding the market.

This is also different from other international conflicts that had less direct influence on energy pricing. The reason the Iran conflict gets so much attention is that oil is a more immediate transmission channel into inflation and rates.

Even so, the current concern points more toward pressure and volatility than toward housing failure.

So Is Now a Bad Time to Buy in Orange County?

Not automatically.

It may be a bad time to buy if the monthly payment would leave you stretched, if your employment situation feels uncertain, if you may need to move again soon, or if you are depending on future refinancing to make the purchase comfortable.

It may be a reasonable time to buy if your income is stable, your cash reserves are solid, the payment works without strain at today’s rate, and you plan to stay long enough for the purchase to make sense beyond the next headline cycle.

That is the key. A scary news environment does not make every home purchase a mistake. But it does punish buyers who are underprepared, overly optimistic about future rates, or shopping without a clear financial margin.

For a cautious first-time buyer in Orange County, the answer is usually not “buy now no matter what,” and it is not “wait because of Iran.” It is closer to this: buy when you are financially ready, when the payment is workable now, and when the home fits a longer-term plan rather than a short-term emotional reaction.

A Quick Note for Orange County Sellers

This is not automatically a bad time to sell either. But it is a worse time to overprice.

About 30% of Orange County active listings had already reduced price at least once in the late-March local report, which reinforces the broader point that pricing discipline matters more in this market. The pricing data also shows a clear pattern. Homes that did not reduce price accounted for most March closings and went pending much faster. Homes that needed reductions took much longer and, on average, sold for less relative to their original ambitions.

That matters because today’s buyers are more payment-sensitive and more analytical than they were when cheap money covered a lot of pricing mistakes.

Sellers can still succeed in Orange County. They just need a cleaner strategy. In this market, precision beats optimism.

Final Takeaway

The war with Iran is a real source of uncertainty, and it can affect the housing market through oil, inflation expectations, and mortgage rates. But based on what Orange County is doing right now, it has not created a market where buyers should automatically wait or sellers should panic.

Inventory has improved. Buyers have more options. Negotiation is more common than it was during the frenzy years. And while rates remain a challenge, the local market is still active and functioning.

So the better question is not whether the headlines are alarming. The better question is whether buying now makes sense for your finances, your monthly budget, and your plans over the next several years. For most cautious first-time buyers in Orange County, the real answer is not “buy now no matter what,” and it is not “wait because of Iran.” It is to buy when the payment works now and the home fits a longer-term plan.

That is the question that leads to better decisions in Orange County, regardless of the current news cycle.

FAQ

Is the Iran conflict likely to crash Orange County home prices?

Current local conditions do not point to a broad crash. The conflict can pressure rates and consumer confidence, but Orange County is still seeing active demand, improving inventory, and a functioning market.

Should first-time buyers wait for mortgage rates to fall?

Only if today’s payment does not work comfortably. Waiting for a lower rate can backfire if competition rises or home prices continue to move up.

Does more inventory mean buyers have the advantage now?

Not a full advantage, but more options than before. Buyers are generally in a better position to compare homes and negotiate than they were during the most competitive years.

Are condos and townhomes more favorable for buyers right now?

In many cases, yes. Attached homes have been moving slower than detached homes in Orange County, which can create a little more flexibility for first-time buyers.

Is this still a good time to sell in Orange County?

It can be, but pricing matters more than ever. Sellers who price to the market are in a better position than sellers who test the market and hope to adjust later.